This a guest contribution by our friend Luke White from Bizval, a professional and independent Chartered Accounting firm delivering business valuations Australia-wide.

Startup valuation is often a very tricky affair.

When a company is in its early growth stages, it can be challenging as there is very little track record to help guide you.

Valuation of companies isn’t just reserved for potential investors or acquisitors.

When founders fail to understand how to properly value their own business, they end up struggling with being under-prepared for investor meetings and unable to justify their venture’s worth (or valuation) to an interested VC (Venture Capital) firm.

Without a proper valuation, your capital raising strategy can be affected drastically.

It’s not uncommon to see founders paying a heavy price for this lack of preparation and know-how.

Traditional Methods for Determining Value

Most well-recognised business valuation methods have a common assumption:

That the business being valued is a going-concern with a sound financial history.

As such, the valuation process often looks backwards to establish a value at a particular point in time.

- Generally, business valuations are conducted by applying one of four commonly accepted valuation methods:

- Capitalisation of Earnings,

- Discounted Cash Flow,

- Net Asset Backing, or

- Industry-Specific method.

The Capitalisation of Earnings and Discounted Cash Flow methods are based on an ‘Earnings Approach’.

The Net Asset Backing method is an ‘Asset Approach’.

Industry-Specific methods fall under ‘Market Approach’.

Of the four traditional methods, only the Discounted Cash Flow approach, might be applicable when doing a startup valuation.

Valuation during the Start-Up Phase

The fundamental driver for a startup valuation is the need to demonstrate the capacity to generate a return for the investors from whom the business is endeavouring to secure funds.

Traditional methods of valuing a business often assume the firm is a “going concern” with a track record of performance or has solid forward projections upon which to rely.

In many instances, established valuation methods simply could not be applied to a start-up scenario.

- In response, different methods were developed, including five we discuss here:

- Berkus Method

- Scorecard Method

- Risk Factor Summation Method

- Venture Capital Method

- First Chicago Method

These methods may be divided into two groupings.

The first group is more suited to valuing pre-revenue startups. The Berkus, Scorecard and Risk Factor Summation Methods each attempt to address the subjective (and frequently over-optimistic) nature of financial forecasts.

The second group tends to be of greater value to investors entering later in the development cycle rather than in the early speculative pre-revenue stages.

Both the Venture Capital and First Chicago Methods are variations on the existing Discounted Cash Flow (DCF) Method.

Following is an overview of the various startup valuation methods.

Berkus Method

The Berkus Method of startup valuation was developed by prolific angel investor David Berkus for application to pre-revenue startups.

His approach was developed in the 1990s and places a value on qualitative aspects of a startup.

Berkus has stated that fewer than one in a thousand startups meet or exceed their projected revenues in the periods planned.

Consequently, his method ignores the founder’s revenue and profit projections.

In addition, the investor/valuer must be of the belief that the company will reach $20mil in revenue by the fifth year.

- The five key elements in the Berkus method are:

- Sound Idea (basic value)

- Prototype (reducing technology risk)

- Quality Management Team (reducing execution risk)

- Strategic Relationships (reducing market risk)

- Product roll-out or Sales (reducing production risk)

A value is assigned to each of the five elements. Then these values are combined to derive the start-up valuation.

| Characteristics | Add to Pre-money Valuation |

|---|---|

| Sound Idea (basic value) | Up to $0.5 million (or 20% of benchmark) |

| Quality Management Team (reducing execution risk) | Up to $0.5 million (or 20% of benchmark) |

| Prototype (reducing tech risk) | Up to $0.5 million (or 20% of benchmark) |

| Strategic Relationships (reducing market risk) | Up to $0.5 million (or 20% of benchmark) |

| Product Rollout or Sales (reducing production risk) | Up to $0.5 million (or 20% of benchmark) |

| Total Pre-Money Valuation | Up to $2.5 million (or your selected benchmark) |

Scorecard Method

This method was developed by angel investor Bill Payne and is also known as the Bill Payne method. Key is a comparison between the target business and other similar start-ups.

Ignoring subjective financial forecasts, the first step when applying the Scorecard Method is to determine the average pre-money valuation of pre-revenue companies in the region and business sector of the target company. Without a thorough involvement in the industry, this could be difficult in Australia (it is a lot easier in the United States where this information is more accessible).

- Once you have this average valuation, adjustments are made by comparing the start-up to the perception of other startups within the same industry. Factors compared are:

- Strength of the Management Team (0–30%)

- Size of the Opportunity (0–25%)

- Product/Technology (0–15%)

- Competitive Environment (0–10%)

- Marketing/Sales Channels/Partnerships (0–10%)

- Need for Additional Investment (0–5%)

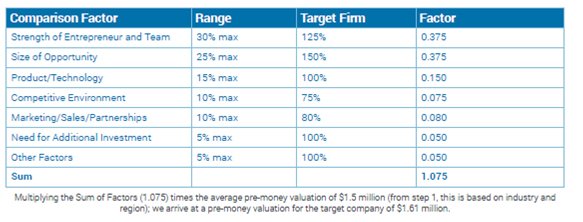

The final valuation amount is calculated by applying these adjustments to the original ‘average’ valuation amount from step one. Following is an example of this calculation, assuming an average pre-money valuation of $1.5mil.

| Comparison Factor | Range | Target Firm | Factor |

|---|---|---|---|

| Strength of Entrepreneur and Team | 30% Max | 125% | 0.375 |

| Size of Opportunity | 25% Max | 150% | 0.375 |

| Product/Technology | 15% Max | 100% | 0.150 |

| Competitive Environment | 10% Max | 75% | 0.075 |

| Marketing Sales/Partnerships | 10% Max | 80% | 0.080 |

| Need for Additional Investment | 5% Max | 100% | 0.050 |

| Other Factors | 5% Max | 100% | 0.050 |

| Sum | 1.075 |

Like the Berkus Method, the Scorecard Method ignores revenue forecasts.

The problem with this method though is that the initial step of finding average startup valuations in the area/industry is very difficult.

Secondly, even with this data, one then needs to compare the target company with other start-ups, in order to undertake this step, one would need a very thorough knowledge and understanding of their local startup market.

Risk Factor Summation Method

This method of startup valuation is often favoured when considering pre-revenue start-ups in the pre-money stage.

Like the Scorecard Method, it starts with the average pre-money valuation of pre-revenue companies in the region and business sector of the target company.

Once the average value of pre-revenue and pre-money start-ups has been determined, it is then adjusted for 12 standard risk factors.

- This method forces investors and valuers to consider the various areas of risks which a venture must manage in order to achieve success. The 12 risk factors are:

- Management

- Stage of the business

- Legislation/Political risk

- Manufacturing risk

- Sales and marketing risk

- Funding/capital raising risk

- Competition risk

- Technology risk

- Litigation risk

- International risk

- Reputation risk

- Potential lucrative exit

Values are attributed to each of the above factors, which in turn are added/deducted from the average to determine the final valuation amount.

Venture Capital Method

The Venture Capital Method of startup valuation looks at what an investor (e.g., venture capitalist) requires in return for their investment and so tends to be of greater value to investors entering later in the business development cycle.

The VC Method was first described by Professor William Sahlman at Harvard Business School in 1987.

The first step is to estimate the terminal value of the business at some point in the future, for example, 5 years.

The terminal value is the return the investor receives when they exit the company (eg – sell their shares).

The selling price can be estimated by determining an expected revenue level and then applying industry-specific profit margins.

Finally, broad-based earnings multiples are applied to the estimated net earnings.

For example, a SaaS company is expected to reach revenue of $30mil in 5 years. Average net earnings for software companies might be 20%, so a net profit of $6mil is used.

Industry-specific earnings multiples for SaaS businesses are then applicable to the estimated profit.

Let’s assume 7x earnings, resulting in an estimated terminal value of $42mil ($6mil x 7).

The second step is to compensate for the high risk involved with investing in start-ups.

Let’s say the investor requires a return of 20x their investment within the five-year timeframe.

This would value the company at $2.1mil post-money ($42mil / 20). If the founder and investor agreed on an investment of $500,000, this result in a pre-money valuation of $1.6mil ($2.1mil less $500k).

Note: the above example does not include any allowance for dilution.

First Chicago Method

The First Chicago Method for startup valuation is essentially a variation on the Discounted Cash Flow method, constructed by combining three scenarios: Best Case, Base Case and Worst Case.

It tends to be of greater value to investors entering later in the development cycle rather than in the early speculative pre-revenue stages.

This method supports the established premise that the value of a financial asset is the discounted value of its future cash flows.

To that extent, it aligns closely with established valuation theory and practice.

However, it is still subject to the high sensitivity of the data being input in the model, although somewhat mitigated with the use of three scenarios.

Wrapping up

Regardless of methodology, or the quality of the financial information, the important thing is for entrepreneurs and founders to validate their conclusions by drawing upon a range of professional advice.

Whether that be an independent startup valuation, the assistance of an expert Accountant like Fullstack Advisory, or a lawyer to review intellectual property and patent laws, the small cost in acquiring professional help early on could prove to be a very worthwhile investment in the long run.

- A professionally prepared valuation can provide an independent perspective in the following situations:

- Investor Funding & Capital Raising.

- Corporate Restructure due to partnership changes or share transfer to a related party.

- Taxation (e.g. when the legal structure of a business changes, it triggers a capital gains tax event, requiring the market value of the business to be determined).

- Employee Share Scheme, Share Gifting or Transfer.

- Dispute Resolution or Litigation

- Migration

When it comes to valuing start-ups, there is no simple or single answer.

Despite the best efforts of Investors and Venture Capitalists, a precise, commonly accepted method for valuing early-stage companies is lacking.

The subjective, often overly optimistic, nature of financial forecasts provides at best a shakyfoundation for a solid outlook.

The challenge is compounded by the many variables to consider: required Terminal Value, what value to place on Goodwill and the experience of the management team to name but a few.

To learn more about obtaining a valuation for your business get in touch with the team at Fullstack Advisory or visit Bizval directly.